Recently, major central banks have revised their monetary policy structures to signal that they will tolerate higher and longer-lasting inflation, arousing much discussion in the market. For example, in August 2020, the US Fed introduced “average inflation targeting,” allowing the inflation rate to exceed the 2% target for a period of time without immediate tightening. This means that it no longer uses the “preemptive strike” policy model, and its tolerance for inflation temporarily above the target has been systematically increased. In July 2021, the European Central Bank (ECB) also revised its inflation target from “close to but slightly below 2%” to a medium-term target of 2% that allows for symmetrical fluctuations, clearly declaring that 2% is not the upper limit, and allowing domestic inflation to fluctuate moderately around 2% for some time.

Fed: recent inflation is transitory

The reason the Fed and ECB have revised their monetary policy structures is the continued low inflation since the global financial crisis. They hope to increase inflation expectations to achieve their inflation targets. The Bank for International Settlements (BIS) observed that the extremely low interest rates and unlimited QE policies around the world have not only caused stock and real estate prices to surge, but also more recently, looking at data in more than 30 countries, caused global inflation rate to increase – in some countries significantly more than expected. For example, the core Personal Consumption Expenditure (PCE) price index, closely watched by the Fed, has continued to rise in recent months, reaching 3.5% in June 2021, far exceeding the inflation target, reaching a high last seen in 1992. In July, the Eurozone’s inflation index and the HICP increased to 2.2%, and the UK’s CPI increased by 2.5%, both exceeding the 2% inflation target. The Fed has repeatedly emphasized that the recent increase in inflation is mainly due to short-term factors such as the economic rebound following the pandemic, supply chain bottlenecks, rising commodity prices, and labor shortages. The most important question is whether this is a short-term phenomenon or the start of a trend.

Our view is that even if these short-term factors do not continue, these signs of loosening of the long-term structural factors that have maintained price stability for decades are the main cause of possible long-term inflation. One of these important structural changes has been to modify the monetary policy structure of major central banks and increase their tolerance for inflation. In particular, in an extremely loose monetary environment, increased dovishness will weaken the central bank’s credibility against inflation and may shake the long-term anchor of stable expectations. Increased inflation expectations would bring about fundamental changes and reverse the stability of the past few decades.

Yellen: It’s a mystery why inflation hasn’t risen with the economy

This article will analyze the source of global price stability over the past 30 years, whether the long-term structural factors that have stabilized or curbed inflation in the past continue to play a role, there are any signs of loosening, and whether a sharp rise in inflation might be triggered at a certain critical point. Clarifying these issues will help us to discuss whether this unprecedented funding frenzy will reverse the price stability of the past few decades, which would lead to serious inflation.

The last time major central banks implemented QE measures was after the 2008 global financial crisis. During the crisis, US GDP fell by 10% compared to the pre-crisis period, but the inflation rate only briefly dropped by about 1.5%, and then stabilized. The Eurozone was also in a similar situation, showing a phenomenon of “Missing deflation” (Balland Mazumder, 2011). Subsequent rounds of QE injected trillions of dollars into the global economy. Economies gradually recovered, and the unemployment rate in the United States dropped below 5%. However, the inflation rates in the US, the Eurozone, and Japan have never been able to reach the 2% inflation target, causing a phenomenon of “missing inflation.” At the time, Fed Chairman Janet Yellen said that it was a mystery why the inflation rate had failed to rise with the economic recovery.

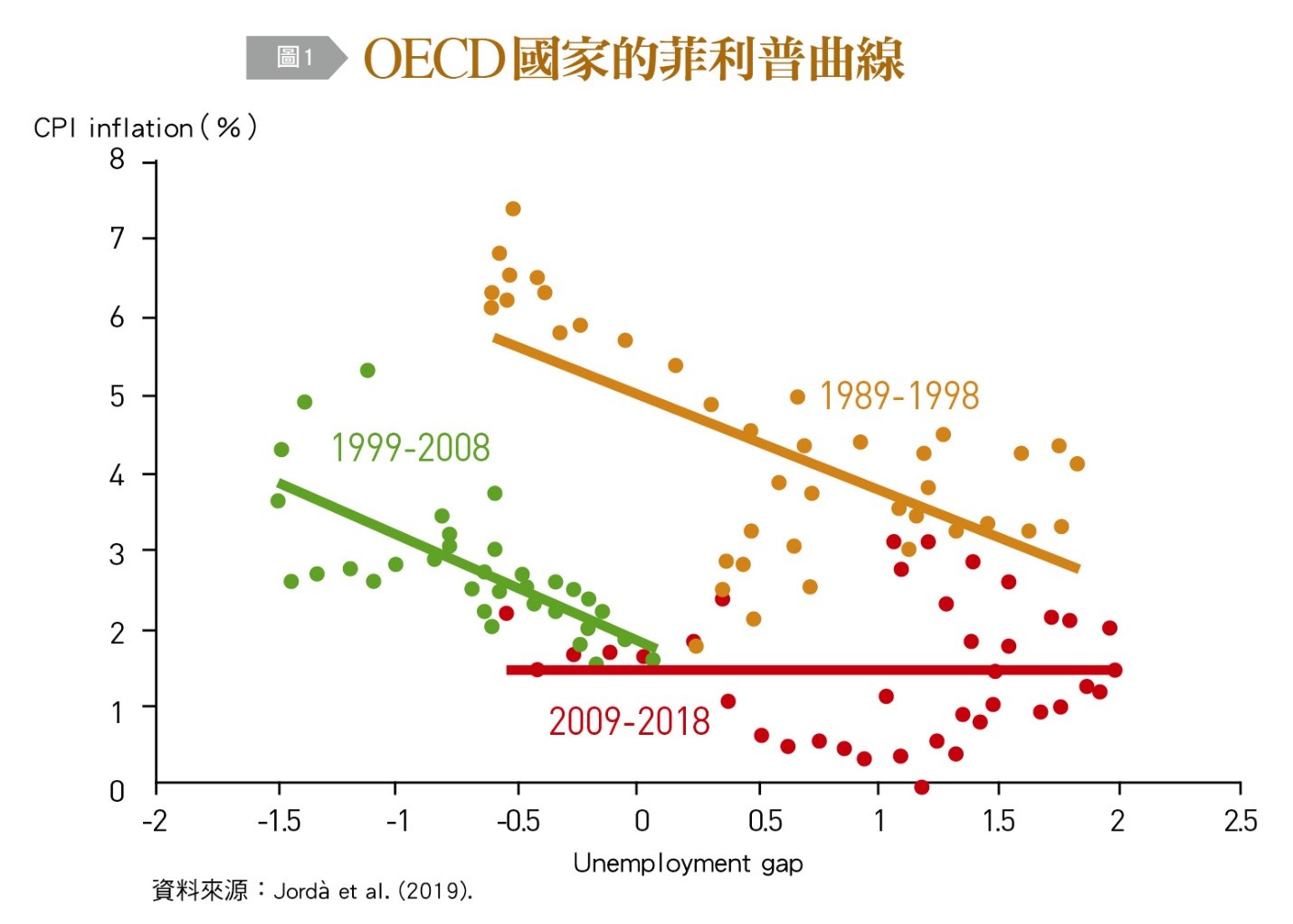

The missing inflation is becoming harder to miss

The decreased sensitivity of the inflation rate to changes in economic activity or the unemployment rate shows that the trade-off relationship between inflation and unemployment has disappeared. This phenomenon is reflected in the flattening of the Phillips Curve. Jordà et al. (2019) used data from Organization for Economic Cooperation and Development (OECD) countries to draw Phillips curves for every 10 years since 1989 (Figure 1). In the first two periods (1989-1998 and 1999-2008), the unemployment rate and inflation still showed a negative relationship, but as time went by, the Phillips curve gradually moved inward and further flattened. In the most recent period (2009-2018), the ten years since the financial crisis, despite the QE implemented by major central banks, the Phillips curve has become almost horizontal. The inactivation of the inflation reaction has caused extensive discussion. This “disappearing inflation” has become increasingly significant over time.

As early as the early 2000s, many studies pointed out that since the mid-1980s, the slope of the Phillips curve in many countries had begun to show a downward trend (Atkesonand Ohanian, 2001; Staigeretal, 2001; Roberts, 2006; Bean, 2006). Kuttner and Robinson (2010) used American data to estimate the slope of the curve over time, and found that it has been decreasing by year since the early 1980s. Zheng Hanliang and Mao Qingsheng (2013) and Liu Shumin (2011) used Taiwanese data and found that Taiwan’s Phillips curve has also flattened. The period from the mid-1980s until the financial crisis was called the Great Moderation. Major countries showed sustained growth with low volatility, and low and stable inflation, in sharp contrast with the previous period of high inflation from the 1970s to the early 1980s.

Five factors for global price stability over the past 30 years

What are the forces behind the low and stable inflation that drove the Great Moderation? Several main factors can be distilled from the large literature discussing the reasons behind the stabilization of inflation and the flattening of the Phillips curve during this period.

(1) Companies are less price-sensitive due to globalization

The reduction in barriers to cross-border outsourcing and trade, and the globalization of the supply chain, have increased international competition, making companies less able to pass on cost pressures. At the same time, emerging economies such as China and India have joined the global labor force, restraining wage growth and inflation. Many studies argue that the effect of globalization is the most important factor flattening the Philips curve (Borio and Filardo, 2007; Del Negro et al., 2020; Razin and Loungani, 2007; Bean, 2006. Del Negro et al. (2020) examined why U.S. prices have been so stable since the 1990s, finding that the main reason is that companies’ pricing decisions have become less cost-sensitive. That is, when total demand rises, production input costs increase, but this does not drive them to increase the price of their products. In addition, various forms of outsourcing have formed a global supply chain, causing structural changes in the labor market, reducing the bargaining power of labor, and thus weakening the trade-off between output and inflation (Stansbury et al., 2020; Lombardi et al., 2020).

(2) A significant increase in the elderly labor force

The trend of automation, the weakening of labor unions, and changes in the demographic structure all have the effect of suppressing wages and inflation. Mojon and Ragot (2019) used data from OECD countries to analyze how demographic changes affect inflation and found that the increased participation rate of the elderly labor force due to the aging population has reduced the pressure on rising wages. The Bank of Japan (2018) estimated that the elasticity of (part-time) elderly labor supply in Japan is twice that of men aged 15 to 64, indicating that when labor demand rises, the elderly are more willing than other groups to join the labor market. Data show that the elderly labor force participation rate has indeed increased significantly over the past ten years, which has suppressed wages. Thus, Japan’s changed demographic structure can explain why its unemployment rate has continued to decline, but wages have stagnated. This is one of the main reasons for its long-term deflation.

(3) The rapid growth of e-commerce, restraining commodity and labor prices

The fierce price competition between physical stores and online merchants and stores, as well as the price transparency it has brought, have helped depress the prices of goods and services – a phenomenon known as the “Amazon effect.” Cavallo (2018) found that Amazon uses a highly flexible pricing strategy, forcing physical stores to respond more quickly and adjust their pricing, even at the expense of profits. An important change he observed is that the frequency of price adjustments in physical stores has accelerated: excluding sales, US physical stores adjusted their prices approximately every 6.7 months during the period from 2008-2010, but every 3.65 months during the period from 2014-2017. While compressing profits, the price competition from e-commerce also inhibited physical retailers from increasing their prices, keeping inflation relatively low. The Bank of Japan also believes that the rise of online shopping is one of the main reasons curbing inflation in Japan. Although Japan’s e-commerce accounts for only 6% of overall retail sales, and online retail transactions are not included in Japan’s CPI, e-commerce has forced physical retailers to lower their prices to stay competitive. This effect has reduced Japan’s core CPI 0.1-0.2 percentage points.

(4) Central banks have paid more attention to controlling inflation than before

Past and current Fed officials, including John Roberts (2006, John Williams (2006), Frederic Mishkin (2007), Ben Bernanke (2007), James Bullard (2018), and Jerome Powell (2019), etc., have all at different times attributed the low and stable inflation and expectations thereof in the US and other major economies over the past few decades to central bank monetary policies, guiding expectations to anchor of long-term expectations. At the same time, as the central bank’s credibility against inflation has been gradually established, expectations have stabilized, making the actual rate less sensitive to changes in unemployment.

(5) After the financial crisis, counter-cyclical product and service inflation remained low

Other studies have examined the price changes of various goods and services from individual data, rather than just looking at overall price trends. Mahedy and Shapiro (2017) used US data to disassemble the core PCE product and labor basket, and estimated a Phillips curve for each category. The results showed that 42% of the core PCE categories were pro-cyclical, and 58% were counter-cyclical. They found that after the financial crisis, as the economy gradually stabilized, inflation in counter-cyclical goods and services remained sluggish. Therefore, low price growth in counter-cyclical goods and services was one of the main reasons for the “missing inflation” following the crisis. It is worth noting that in addition to the characteristics of individual markets, products and services with counter-cyclical inflation are more likely to be affected by policy or government regulation, causing their prices to change outside of overall economic trends. If the policy is changed so that these counter-cyclical items then become pro-cyclical, the overall inflation rate will rise.